Foreign investment inflows in markets hit record high on JPMorgan boost

MUMBAI

:

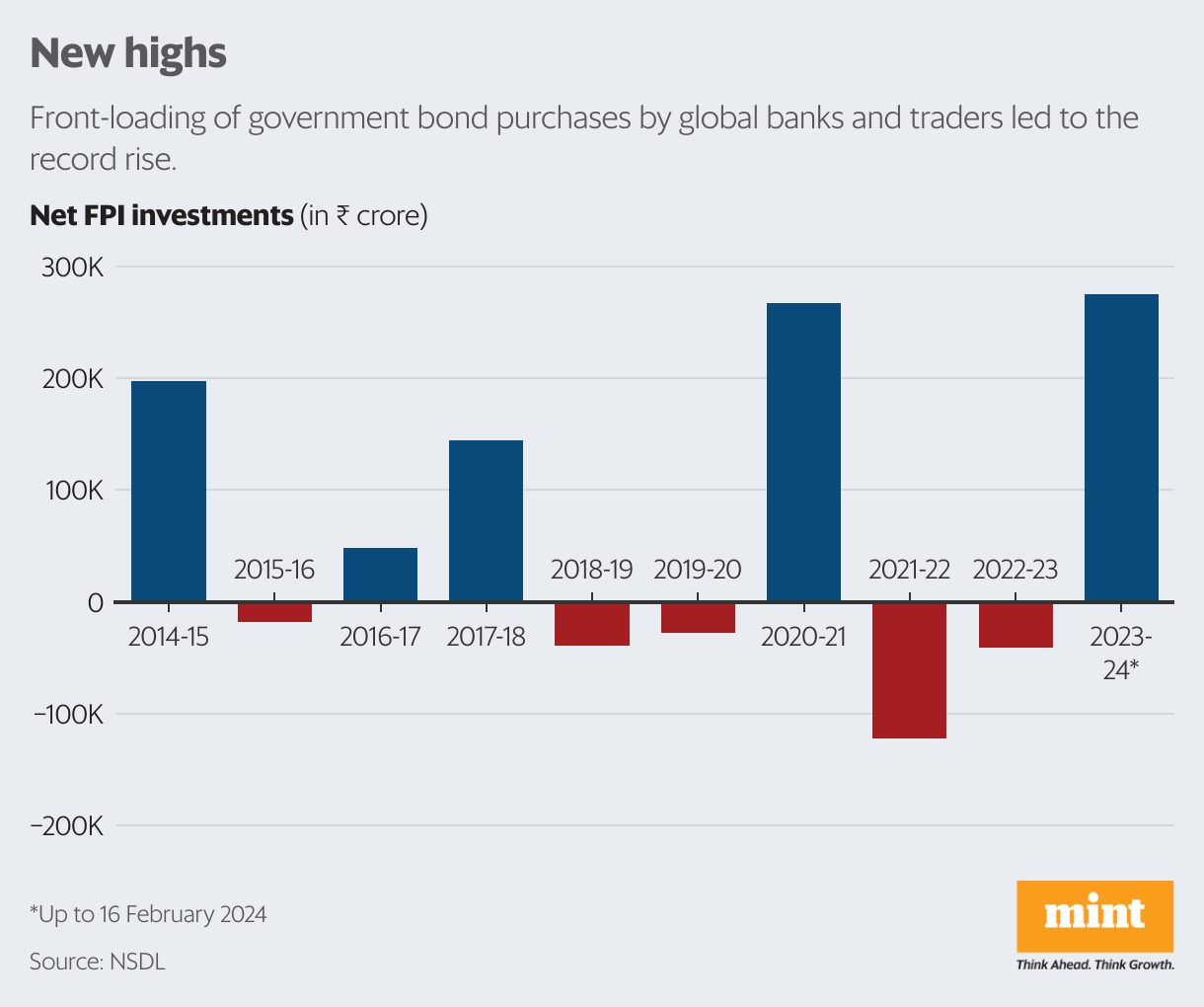

Overall inflows from foreign investors have hit a record high of ₹2.74 trillion this fiscal year, chiefly due to front-loading of government bond purchases by global banks and traders.

This follows JP Morgan’s decision to include Indian government bonds in its government bond index-emerging markets (GBI-EM) from June. Market experts say the move could attract $25 billion in inflows from passive trackers such as debt exchange-traded funds (ETFs) and index funds.

The break-up of net inflows this fiscal, as of 16 February, was ₹1.68 trillion into equity, ₹1.01 trillion into debt, a negative ₹0.06 trillion through the debt voluntary retention route (debt-VRR), and ₹0.11 trillion into hybrid instruments, including debt, equity and commodities such as gold, according to securities depository National Securities Depository Limited (NSDL).

Debt-VRR enables foreign portfolio investors to invest in debt markets free of macro-prudential and other regulatory rules applicable to FPI (foreign portfolio investor) investments, provided they voluntarily commit to retain a minimum percentage of their investments in India for a specified period of time, according to law firm Shardul Amarchand Mangaldas.

Apart from the front-loading of bond purchases, expectations of lower interest rates in the second half of FY25 and a relatively stable rupee also attracted foreign investments into debt, fund experts said.

“There are a host of factors for Indian debt turning attractive to foreign investors,” said Ashish Gupta, chief investment officer, Axis Mutual Fund.

“Indian government bonds’ inclusion in the JPMorgan Bond index is one of the main ones, [with the] probable inclusion into the Bloomberg bond index, anticipation of lower interest rates, and a stable currency being the others,” he added.

The rupee has traded in a range of 83.40-81.77 to the US dollar so far this fiscal, against a more volatile 82.99-75.32 over the same period in the previous fiscal year.

Reserve Bank of India (RBI) governor Shaktikanta Das said at the recent rate-setting policy meeting on 8 December that the central bank expects retail inflation to grow at 4% in the second quarter of FY25, down from 5% in the first three months of the next fiscal.

Markets are factoring in a cut in the repo rate, which stands at 6.5% currently, some time in the second half of FY25 as inflation moderates towards RBI’s comfort target of 4%.

According to Nilesh Shah, group president and managing director at Kotak Mahindra AMC, the frontloading of government bonds purchases by global banks and traders was the key reason for the “robust” FPI debt flows.

He said around $5 billion have been invested in Indian debt so far this fiscal year, with another $6-7 billion expected through June ahead of the JPMorgan Bond index inclusion, after which passive trackers such as debt ETFs and index funds are expected to invest $25 billion through March 2026.

U.R. Bhat, co-founder of Alphaniti Fintech, said the preference for active funds is primarily for the long dated 10-year government bond, whose coupon is higher than that of shorter tenure bonds, and that the price would rise more than that of shorter tenure ones after RBI cuts the repo rate.