Relief, finally: Sebi lifts the FPI disclosure overhang on market

The stock market watchdog will not force foreign investors that haven’t disclosed their ultimate beneficiaries to sell their holdings beginning 1 February, two people aware of the regulator’s thinking said, lifting a cloud that has hung heavy over the market in the recent past.

While some categories of foreign portfolio investors (FPIs) will be exempt from the new rule on enhanced disclosures, others will get additional time to comply. The rule will also not cover investments in companies that are widely owned with no clear promoter.

This means there is no 1 February cliff for FPIs that have not complied with Securities and Exchange Board of India’s (Sebi) new rules mandating enhanced disclosures.

“FPIs that may be required to provide enhanced disclosures are expected to be significantly less than estimated in the consultation paper and the Sebi board note. Exemption from enhanced disclosures have been provided to FPIs that are sovereign wealth funds (SWFs), listed companies on certain global exchanges, public retail funds, and other regulated pooled investment vehicles with diversified global holdings,” said one of the two people cited above.

FPIs that met the criteria for enhanced disclosures as of 31 October 2023 were given time till 31 January 2024 to rebalance their holdings, the people said. If these FPIs continue to meet the criteria for enhanced disclosures as of January-end, they will get 10-30 more days to provide more details.

“Even thereafter, if they fail to provide any details, they would have a further six months to r.educe their holdings,” the second person added.

The disclosure rule will not apply to investments in companies with no identified promoter. Some of the listed entities with no clear promoter and large FPI holdings include HDFC Bank Ltd, ICICI Bank Ltd and ITC Ltd.

“The norms should be eased in a manner to make them easy to comply with over a given time frame, without diluting their substantive features,”said Nirmal Jain, the founder of IIFL Group. He added that one of the “negative overhangs” for the market would be done away with following the Sebi clarification.

Sebi mandates listed companies to have a minimum public shareholding (MPS) of 25%. Regulators have long worried that some promoters bypass this rule by investing through FPIs close to them. The matter blew up in the wake of the Hindenburg report in January 2023, which alleged that promoters were behind some of the FPIs that invested in Adani group companies. The Adani Group denied the allegations.

In May 2023, Sebi issued a consultation paper mandating additional FPI disclosures, and its board approved them in June. Now, any fund owning over 50% of its assets under management in a single corporate entity, or above 25% of assets in the Indian market, should provide granular details of ultimate beneficial owners (UBO).

The enhanced disclosure norms tighten access to the Indian market through participatory notes (P-notes). Many funds that want to avoid registering with Sebi can access the Indian market through another registered FPI, which issues a P-note to that entity. While the P-note issuer is known, granular details of the ultimate owner are not verifiable currently. The new regulation will make it inexpedient for anybody wanting to work around the MPS norms by hiding behind a registered FPI as P-notes will also have to be accompanied by details of its ultimate owner.

“The UBO issue needs to be resolved at the earliest,” said Chirag M. Shah, a securities lawyer. “The current overhang is not good; it will sully the exuberance that is otherwise based on solid economic transformation. Time extension for compliance and exempting entities such as SWF and other entities of similar pedigree would be desirable. Equally, investors in companies with wide institutional ownership and no identifiable promoters should also be exempted,” Shah added.

However, some market participants didn’t agree that the UBO norm deadline had impacted FPI flows.

“Flows are guided by fundamental factors such as earnings, which for the large caps have been very average, to say the least,” said Shankar Sharma, the founder of GQuant Investech, adding “attributing the recent FPI selling to the UBO norms is an exercise in futility”.

Provisional FPI net inflows at a negative ₹6,934.93 crore on Wednesday seemed to support Sharma’s assertion. To be sure, FPIs closed out their negative bets on Nifty and Bank Nifty futures to a cumulative 8,556 contracts on Wednesday from 18,829 contracts a day earlier. Closing out shorts added some heft to the provisional domestic institutional investor (DII) inflows of ₹6,012.67 crore. The National stock Exchange’s 50-share Nifty closed 1% higher on Wednesday.

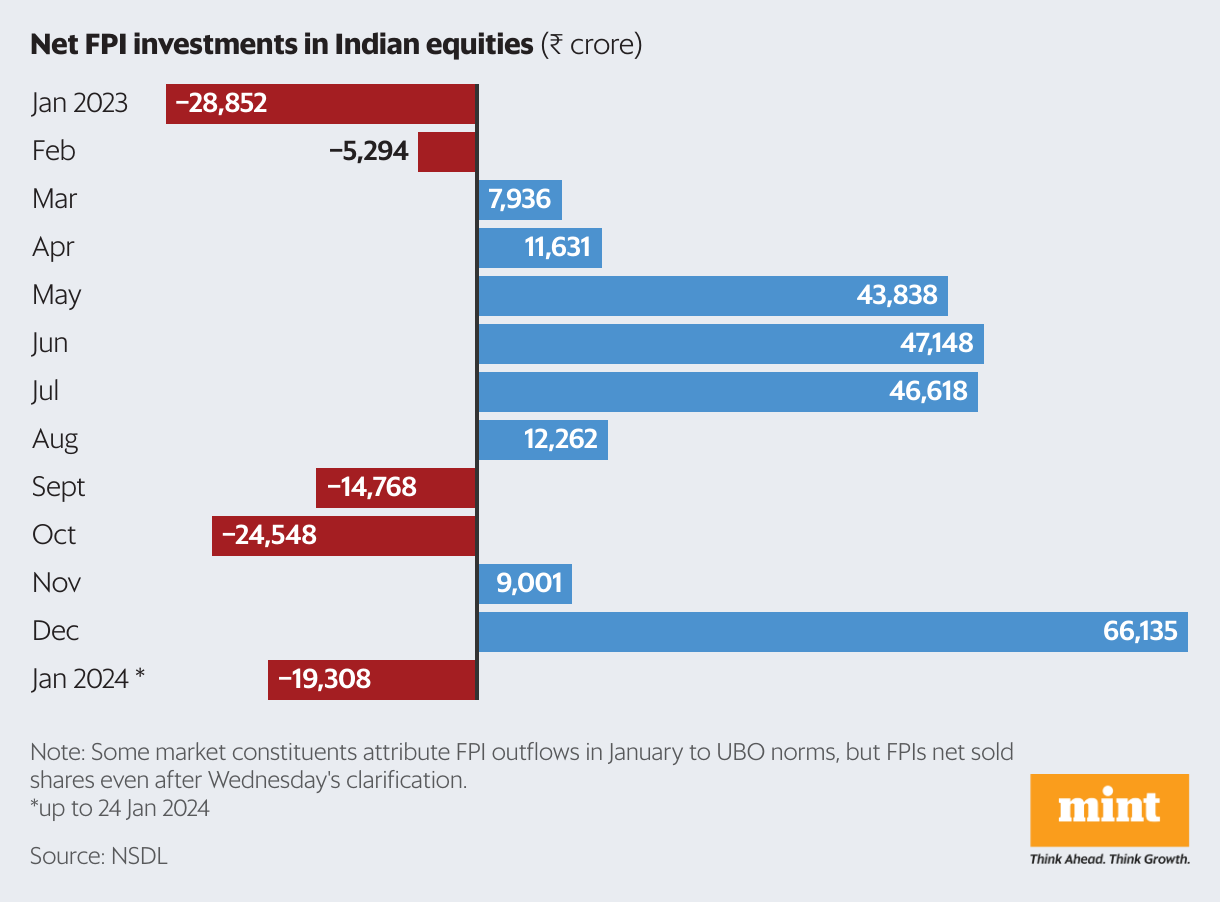

After buying shares worth ₹1.71 trillion in the calendar to December 2023, FPIs have sold shares worth ₹19,308 crore in January so far. One of the reasons, apart from disappointing results from bluechips such as HDFC Bank, Infosys and Hindustan Unilever, was the looming deadline that was estimated to affect ₹2.5 trillion of holdings held by specified FPIs.