Volume, margin moves to pave way for VRL Logistics

Multiple factors are driving VRL Logistics Ltd’s robust growth, demonstrated by a notable 36% surge in its shares so far this calendar year. The logistics company’s success is rooted in its strategic expansion of fleet capacity, an expanding customer base, and capturing market share from less organized competitors.

Further upsides hinge on the trajectory of volumes and margins. And for that, the company seems to be making the right moves. VRL’s volume growth is expected to be driven by branch additions across various geographies, setting the stage for continued success.

Emkay Global Financial Services, in their 1 December report, said that VRL’s history of careful branch expansion, ensuring utilization and profitability, “lends comfort to our forecast of ~120 net-branch additions a year, till FY26E. With higher visibility on volumes in light of formalization of the PTL (partial-truck load) industry, VRL is now adding higher-capacity vehicles (~23%) to further improve profitability per truck.”

Another positive development is the recent uptick in freight rates, combined with stable diesel prices at around ₹89 per litre, enhancing prospects of profitability for truckers like VRL.

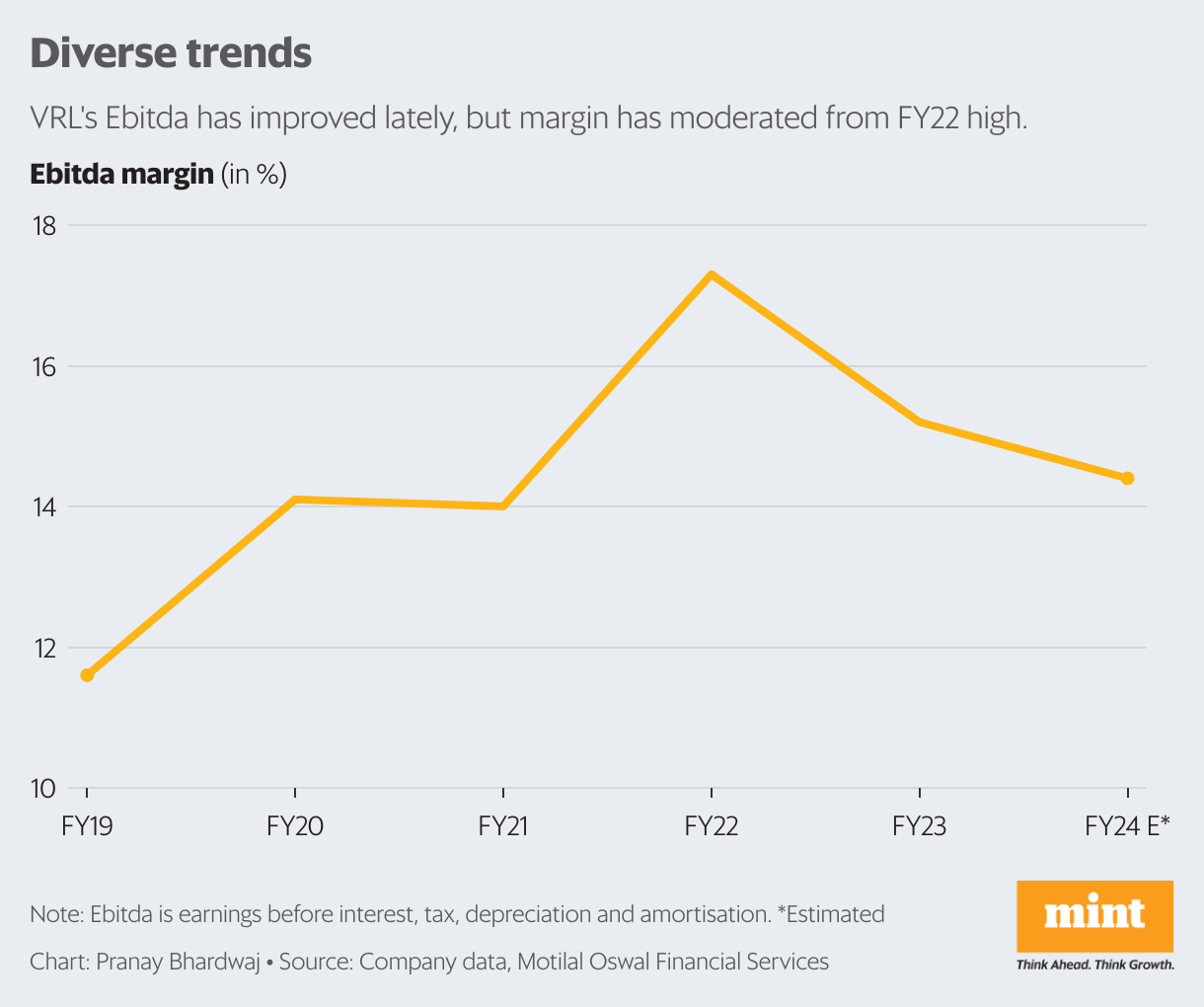

Furthermore, in FY23 and the first half of FY24, VRL divested its non-core businesses to focus on goods transportation or less than truckload (LTL) operations. This shift comes as the government intensifies compliance in the logistics sector, favouring established companies. Plus, the LTL segment, transporting shipments from multiple customers in a single vehicle, commands high margin.

“The goods transportation segment enjoys an average Ebitda margin of about 15-16%, outperforming peers,” pointed out Ankita Shah, vice president of research – Institutional Equities at Elara Capital. This advantage stems from owning rather than leasing trucks, and partnerships with petrol pumps that help reduce costs and enhance margins, Shah added.

Against this backdrop, analysts believe that the management’s guidance of a 15-16% Ebitda (earnings before interest, tax, depreciation and amortization) margin for FY24 is within reach. In the first half of FY24, VRL reported a 9% year-on-year increase in its revenue, accompanied by a 9.5% growth in volumes. This performance was primarily driven by expanding branch network and acquiring new customers. The second half of the fiscal year looks promising, with expectations of improved realizations and growth driven by the festive season.

Currently, the VRL stock trades at 27 times its FY25 earnings, according to Bloomberg data. While the valuations are not too demanding, potential risks include failure to implement freight hikes, offering discounts on new routes, and rising diesel costs.

The possibility of a shift to rail transport with the introduction of dedicated freight corridors could also impact the company’s growth.